Comparing High-Yield Savings Accounts: Finding the Best Rates Above 5% for Your Emergency Fund

In today’s dynamic financial landscape, simply stashing your cash in a traditional savings account is akin to leaving money on the table. With inflation steadily eroding purchasing power, it’s more crucial than ever to make your money work harder for you. This is where high-yield savings accounts come into play, offering significantly better interest rates than their conventional counterparts. For those diligently building an emergency fund, finding the best rates, especially those above 5% APY, can make a substantial difference in achieving financial security and growth.

An emergency fund is the cornerstone of a robust financial plan. It acts as a safety net, providing a buffer against unforeseen expenses like medical emergencies, job loss, or unexpected home repairs. However, merely having an emergency fund isn’t enough; it needs to be accessible, liquid, and ideally, growing. This is precisely why a high-yield savings account for your emergency fund is an intelligent choice. It provides the liquidity you need while simultaneously helping your money combat inflation and accumulate interest.

This comprehensive guide will delve into the world of high-yield savings accounts, focusing on how to identify the best options that offer interest rates above 5%. We’ll explore the critical factors to consider when choosing an account, highlight some of the top contenders in the market, and provide practical tips to maximize your savings. Our goal is to empower you with the knowledge to make an informed decision, ensuring your emergency fund not only provides peace of mind but also grows effectively.

What Are High-Yield Savings Accounts (HYSAs)?

Before we dive into the specifics of finding rates above 5%, let’s establish a clear understanding of what high-yield savings accounts (HYSAs) are. In essence, HYSAs are savings accounts that offer significantly higher annual percentage yields (APYs) compared to traditional savings accounts offered by brick-and-mortar banks. While a typical savings account might offer a meager 0.01% to 0.05% APY, HYSAs can offer rates that are ten, twenty, or even fifty times higher.

The primary reason for these higher rates often lies in the operational model of the institutions offering them. Many HYSAs are provided by online-only banks or credit unions, which have lower overhead costs compared to traditional banks with extensive branch networks. These cost savings are then passed on to consumers in the form of more attractive interest rates. Additionally, some institutions use HYSAs as a way to attract deposits, which they can then use for lending or other investment activities.

Key characteristics of HYSAs include:

- Higher Interest Rates: This is the most defining feature. The interest earned compounds over time, meaning you earn interest not only on your initial deposit but also on the accumulated interest.

- Liquidity: Unlike certificates of deposit (CDs), HYSAs generally offer easy access to your funds. You can typically withdraw money as needed, though some accounts might have limitations on the number of monthly transactions.

- FDIC or NCUA Insurance: Most reputable HYSAs are insured by the Federal Deposit Insurance Corporation (FDIC) for banks or the National Credit Union Administration (NCUA) for credit unions, up to the standard maximum deposit insurance amount of $250,000 per depositor, per institution, for each account ownership category. This provides a crucial layer of security for your deposits.

- Online-Centric: A significant number of HYSAs are offered by online banks, meaning most, if not all, banking activities are conducted digitally. This can include account opening, deposits, withdrawals, and customer service.

- Minimal Fees (Often): Many HYSAs boast low or no monthly maintenance fees, especially if certain conditions are met (e.g., maintaining a minimum balance, setting up direct deposit).

Understanding these fundamental aspects of high-yield savings accounts is the first step towards leveraging them effectively for your financial goals, particularly for securing and growing your emergency fund.

Why a High-Yield Savings Account for Your Emergency Fund?

The decision to house your emergency fund in a high-yield savings account is a strategic one, offering a multitude of benefits that traditional savings options simply cannot match. When it comes to an emergency fund, the primary goals are safety, accessibility, and growth. HYSAs excel in all three areas.

Firstly, the safety aspect is paramount. As mentioned, most reputable HYSAs are FDIC or NCUA insured. This means that even if the bank or credit union fails, your deposits are protected up to $250,000. This level of security is crucial for funds you cannot afford to lose, such as an emergency reserve.

Secondly, accessibility is a key differentiator. While investments like stocks or real estate might offer higher potential returns, they come with significant volatility and illiquidity. An emergency fund needs to be readily available when unexpected expenses arise. HYSAs provide this liquidity, allowing you to transfer funds to your checking account quickly, often within one to three business days, without penalties for early withdrawal (unlike CDs).

Thirdly, and perhaps most compellingly, is the potential for growth. With interest rates hovering above 5% APY, your emergency fund isn’t just sitting idle; it’s actively growing. This growth helps to offset the effects of inflation, preserving your purchasing power over time. For example, if you have $10,000 in an account earning 5% APY, you’ll earn $500 in interest over a year, assuming no further deposits or withdrawals. In contrast, a traditional savings account at 0.05% APY would only yield $5 over the same period. This difference can be substantial over several years, helping you build a more robust financial safety net.

Consider the psychological benefit as well. Knowing that your emergency fund is not only secure and accessible but also actively generating returns can provide an immense sense of financial peace. It transforms a static pool of money into a dynamic asset, working tirelessly to support your financial well-being.

Key Factors to Consider When Choosing a High-Yield Savings Account

While the allure of a high APY is strong, it’s essential to look beyond just the interest rate when selecting a high-yield savings account. Several other factors can significantly impact your experience and the overall effectiveness of the account for your emergency fund. Here’s a breakdown of what to consider:

1. Annual Percentage Yield (APY)

Naturally, the APY is a primary concern. Our focus here is on finding accounts offering above 5% APY. However, be aware that APYs can be variable and subject to change based on market conditions and the Federal Reserve’s interest rate policies. Always check the current rate and understand if it’s a promotional rate or a standard offering. Some banks might offer a high introductory rate that drops after a few months.

2. Minimum Balance Requirements

Some HYSAs require a minimum balance to open the account or to earn the advertised APY. Others might waive monthly fees if you maintain a certain balance. Ensure that any minimum balance requirements are feasible for your emergency fund. Ideally, you want an account with no minimum balance or one that aligns with your current savings capacity.

3. Fees and Charges

Scrutinize the fee schedule. Common fees include monthly maintenance fees, excessive transaction fees (though HYSAs usually have fewer restrictions than checking accounts), and wire transfer fees. The best high-yield savings accounts have minimal or no fees, ensuring that your earnings aren’t eroded by charges.

4. FDIC or NCUA Insurance

Always verify that the institution is insured by the FDIC (for banks) or NCUA (for credit unions). This protects your deposits up to $250,000 per depositor, per institution, per ownership category. Never deposit your emergency fund into an uninsured account.

5. Accessibility and Transfer Limits

Consider how easily you can access your funds. While HYSAs offer liquidity, some may have limits on the number of withdrawals or transfers you can make per month (often six, due to Regulation D, though this has been temporarily suspended by the Fed for some time, it’s good practice to be aware of potential limits). Also, check the typical transfer times to link external accounts. You want quick access to your emergency fund when needed.

6. Online Banking Experience and Customer Service

Since many HYSAs are offered by online banks, a user-friendly website and mobile app are crucial. Look for features like easy account management, mobile check deposit, and robust security. Excellent customer service, available through various channels (phone, chat, email), is also important in case you encounter issues.

7. Reputation and Financial Health of the Institution

Research the bank or credit union’s reputation. Read reviews, check their financial health ratings if available, and ensure they have a history of reliable service. While FDIC/NCUA insurance protects your money, a financially stable institution provides peace of mind.

8. Integration with Other Accounts

If you prefer to keep all your banking with one institution, check if the HYSA integrates well with other accounts you might have (checking, investments). This can simplify money management.

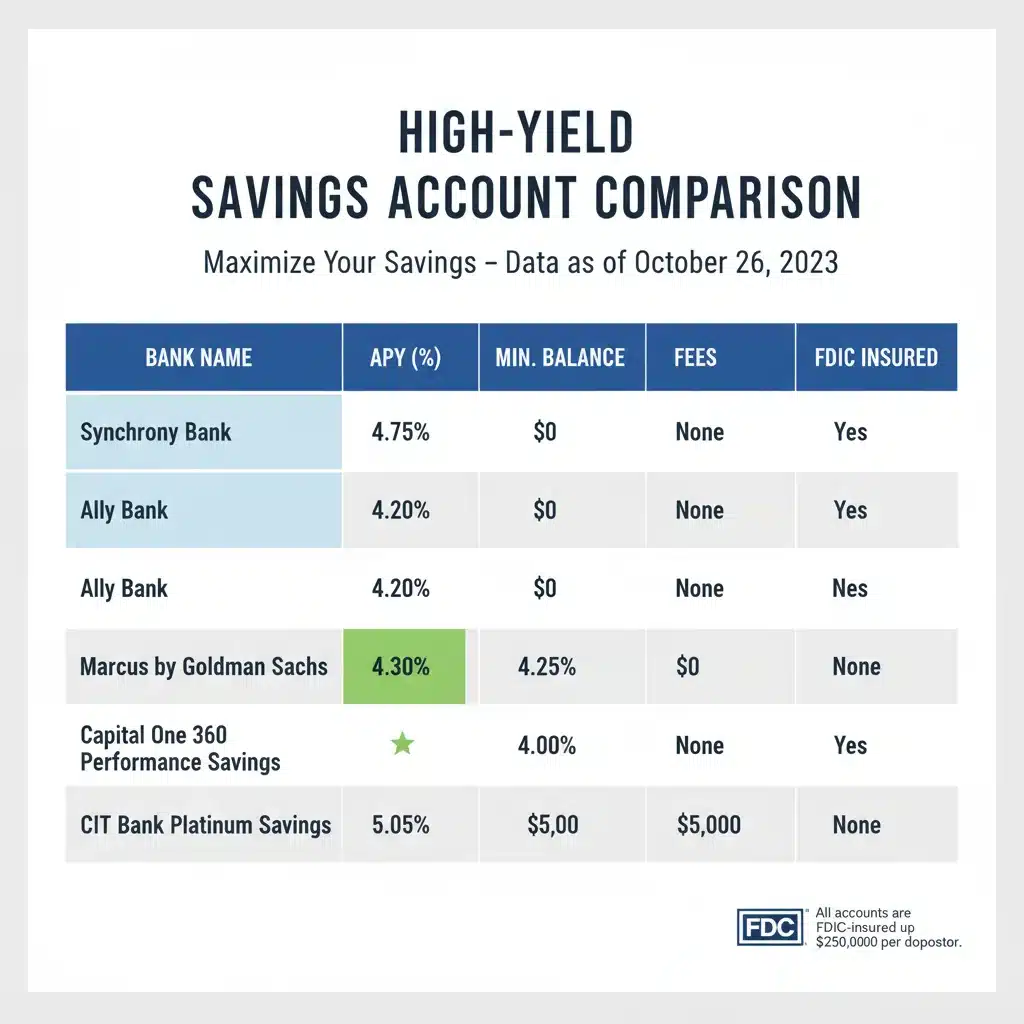

Top Contenders: High-Yield Savings Accounts Above 5% APY

Finding high-yield savings accounts with rates consistently above 5% APY requires careful research, as these rates can fluctuate. However, several online banks and financial institutions are known for offering highly competitive rates. It’s crucial to note that specific rates are subject to change, and you should always verify the current APY directly on the institution’s website.

Online Banks Leading the Way

Online banks often lead the charge in offering the most attractive high-yield savings rates due to their lower operating costs. Here are examples of types of institutions and their typical offerings, which may include rates above 5% at any given time:

- Regional Online Banks/Credit Unions: Smaller, digitally-focused banks or credit unions can sometimes offer very aggressive rates to attract new customers. These might include institutions like PenFed Credit Union (often has competitive rates, sometimes requiring membership criteria), CIT Bank (known for competitive savings rates), or Discover Bank (consistently offers solid HYSAs).

- Fintech Companies with Banking Partners: Some financial technology (fintech) companies partner with FDIC-insured banks to offer savings products. These can include platforms like Wealthfront Cash Account or Betterment Cash Reserve, which often boast very competitive APYs. They often bundle savings with investment features.

- Lesser-Known Online Banks: Don’t overlook smaller, FDIC-insured online banks. They might not have the brand recognition of larger institutions but can offer exceptionally high rates to gain market share. Examples could include Vio Bank, TAB Bank, or UFB Direct. These banks are often among the first to offer rates above the general market average.

Important Considerations for 5%+ APY Accounts:

- Promotional vs. Standard Rates: Always distinguish between a temporary promotional rate and a standard, ongoing APY. A 5% rate might be an introductory offer that reverts to a lower rate after a few months.

- Tiered Rates: Some accounts offer tiered rates, meaning you only earn the highest APY on balances up to a certain amount, or if you meet specific requirements (e.g., direct deposit, minimum number of debit card transactions). Carefully read the terms to understand how the APY applies to your specific balance.

- Membership Requirements: Credit unions, in particular, often require membership. This might involve living in a specific geographic area, working for a certain employer, or joining an affiliated organization.

- Dynamic Market: The market for high-yield savings account rates is highly dynamic. What’s 5% today might be 4.8% next month, or even 5.2% elsewhere. Regularly review your account’s APY and compare it with current market offerings.

To find the most up-to-date rates, it’s advisable to consult financial comparison websites that regularly track high-yield savings rates. Always click through to the bank’s official website to confirm the current APY and terms before opening an account.

Maximizing Your Emergency Fund Growth with HYSAs

Simply opening a high-yield savings account is a great first step, but there are additional strategies you can employ to maximize the growth of your emergency fund and ensure it serves its purpose effectively.

1. Automate Your Savings

The easiest way to grow your emergency fund is to make saving automatic. Set up recurring transfers from your checking account to your HYSA on payday. Even small, consistent contributions add up significantly over time, especially with compounding interest. Treat your emergency fund contributions like any other essential bill.

2. Regularly Review APY and Switch Accounts if Necessary

As mentioned, high-yield savings account rates are not static. Banks constantly adjust their APYs based on market conditions. Make it a habit to review your account’s APY every few months and compare it with the best rates available from other FDIC/NCUA-insured institutions. If you find a significantly higher rate elsewhere with favorable terms, don’t hesitate to switch. The process of transferring funds between HYSAs is usually straightforward.

3. Understand Compounding Interest

Compounding interest is your best friend when it comes to long-term savings. The interest you earn also starts earning interest. The higher the APY and the longer your money stays in the account, the more powerful compounding becomes. This is why even a small difference in APY (e.g., 5% vs. 5.25%) can lead to a noticeable difference in your total savings over several years.

4. Avoid Unnecessary Withdrawals

An emergency fund is for emergencies. While HYSAs offer liquidity, frequent or unnecessary withdrawals can hinder its growth. Each withdrawal reduces the principal amount on which interest is calculated, slowing down the compounding effect. Try to keep your emergency fund intact unless a genuine emergency arises.

5. Consider Laddering if You Have Very Large Funds

For those with exceptionally large emergency funds (e.g., well over the FDIC insurance limit), you might consider a strategy called "laddering." This involves spreading your funds across multiple HYSAs at different FDIC/NCUA-insured institutions. This ensures that all your funds remain protected by insurance and allows you to diversify your exposure to any single bank’s rate changes. However, for most people, keeping their emergency fund within the $250,000 insurance limit at one or two institutions is sufficient.

6. Keep an Eye on Inflation

While HYSAs help combat inflation, it’s worth understanding the real return on your savings. If inflation is 3% and your HYSA earns 5% APY, your real return is 2%. While not as high as your nominal return, it’s still positive and much better than losing purchasing power in a low-interest account. Staying informed about economic conditions can help you make better financial decisions.

Common Questions About High-Yield Savings Accounts

Navigating the world of high-yield savings accounts can bring up several questions. Here are answers to some of the most common inquiries:

Q1: Are high-yield savings accounts safe?

A: Yes, as long as they are offered by FDIC-insured banks or NCUA-insured credit unions. This insurance protects your deposits up to $250,000 per depositor, per institution, per ownership category. Always verify this insurance status before opening an account.

Q2: How often do high-yield savings account rates change?

A: HYSA rates are variable and can change frequently, often in response to changes in the Federal Reserve’s federal funds rate and overall economic conditions. Banks typically adjust their rates within days or weeks of a Fed rate change. It’s wise to check your account’s current APY periodically.

Q3: Are there any downsides to high-yield savings accounts?

A: The main potential downsides are:

- Variable Rates: Rates can decrease, meaning your earnings might fluctuate.

- Online-Only Nature: If you prefer in-person banking services, an online-only HYSA might feel less convenient. However, many online banks offer excellent digital tools and customer support.

- Transaction Limits: While less common now due to Regulation D changes, some accounts might still have limits on the number of free withdrawals or transfers per month.

Q4: How do I transfer money into and out of a high-yield savings account?

A: Most online HYSAs allow you to link external bank accounts (like your checking account). You can then initiate transfers directly from the HYSA’s online portal or mobile app. Transfers typically take 1-3 business days to process. You can also set up direct deposit from your employer or deposit checks via mobile capture.

Q5: Is a high-yield savings account better than a CD for an emergency fund?

A: For an emergency fund, a high-yield savings account is generally preferable to a Certificate of Deposit (CD). While CDs often offer slightly higher rates for locking up your money for a fixed term, they impose penalties for early withdrawals. An emergency fund needs to be liquid and accessible without penalties, which HYSAs provide.

Q6: Do I have to pay taxes on the interest earned?

A: Yes, the interest earned on your high-yield savings account is considered taxable income by the IRS and will be reported to you on Form 1099-INT if you earn more than $10 in interest during the year. You will need to include this income when filing your taxes.

Q7: Can I have multiple high-yield savings accounts?

A: Absolutely! Many people choose to have multiple HYSAs, perhaps with different institutions to take advantage of varying rates, or to segment their savings for different goals (e.g., one for an emergency fund, another for a down payment). Just ensure all accounts are FDIC/NCUA insured.

Conclusion: Secure Your Future with a High-Yield Emergency Fund

In an era where every dollar counts, optimizing your savings is not just a recommendation but a financial imperative. A high-yield savings account offering rates above 5% APY is an incredibly powerful tool for building and maintaining a robust emergency fund. It provides the essential trifecta of security, accessibility, and growth, ensuring your financial safety net is not only there when you need it but also working diligently to increase its value.

By carefully considering factors beyond just the APY, such as minimum balance requirements, fees, FDIC/NCUA insurance, and the overall banking experience, you can select an account that perfectly aligns with your financial needs and preferences. Remember that the financial landscape is constantly shifting, so regular review of your account’s performance and comparison with market leaders is key to maximizing your returns.

Don’t let your hard-earned money languish in a low-interest account. Take proactive steps today to research, compare, and open a high-yield savings account. Empower your emergency fund to grow, protect your financial future, and gain the peace of mind that comes with smart, efficient savings. Your financial well-being is worth the effort.

Bond yield volatility effects on mortgage rates US: risks?

Bond yield volatility effects on mortgage rates US: risks?  Mastering 401(k) Contribution Limits 2026: Your Essential Guide

Mastering 401(k) Contribution Limits 2026: Your Essential Guide  small business lending trends US 2025: what to expect

small business lending trends US 2025: what to expect