Mastering 401(k) Contribution Limits 2026: Your Essential Guide

As we march steadily towards the future, planning for retirement becomes an increasingly critical component of a sound financial strategy. For many, the 401(k) remains the cornerstone of these efforts, offering tax-advantaged growth and a structured path to financial independence. Each year, the Internal Revenue Service (IRS) adjusts the 401(k) contribution limits, reflecting economic shifts and inflation. Understanding these changes, especially the projected 401k contribution limits 2026, is not just about compliance; it’s about optimizing your savings potential and ensuring your retirement nest egg grows as robustly as possible.

The landscape of retirement savings is dynamic, with regulations and economic factors constantly influencing how much you can contribute and how those contributions impact your overall financial picture. For 2026, while official numbers are still subject to final IRS announcements, we can make informed projections based on historical trends and current economic indicators. This comprehensive guide aims to equip you with the knowledge needed to navigate these future limits, strategically plan your contributions, and leverage every available advantage to secure a comfortable retirement.

Whether you’re a seasoned investor or just beginning your retirement savings journey, staying informed about the 401k contribution limits 2026 is paramount. This article will delve into the intricacies of these limits, explore the crucial role of catch-up contributions for older workers, discuss the impact of market conditions, and offer actionable strategies to maximize your retirement savings. We’ll also touch upon the various types of 401(k) plans and how their specific rules might affect your contribution strategy. By the end of this guide, you’ll have a clear roadmap for approaching your 401(k) contributions in 2026 and beyond.

Understanding the Basics of 401(k) Plans and Contribution Limits

Before we dive into the specifics of the 401k contribution limits 2026, it’s essential to have a solid understanding of what a 401(k) plan is and why these limits exist. A 401(k) is an employer-sponsored retirement savings plan that allows employees to invest a portion of their paycheck before taxes are withheld. This pre-tax contribution reduces your taxable income in the year you contribute, offering an immediate tax benefit. The money then grows tax-deferred until retirement, at which point withdrawals are taxed as ordinary income.

The primary purpose of contribution limits set by the IRS is to ensure fairness and prevent high-income earners from disproportionately benefiting from the tax advantages of these plans. These limits are periodically adjusted, primarily to account for inflation, ensuring that the purchasing power of your retirement savings keeps pace with the cost of living. The adjustments are usually based on an inflation index, meaning that as the cost of goods and services rises, so too do the contribution limits, albeit often with a slight lag.

For individuals, understanding these limits is crucial for several reasons. Firstly, contributing up to the maximum allowed limit is often one of the most effective ways to accelerate your retirement savings. Secondly, exceeding the limit can lead to tax penalties, making careful tracking of your contributions absolutely necessary. Lastly, the limits influence your overall financial planning, affecting decisions related to other retirement accounts like IRAs and taxable investment accounts.

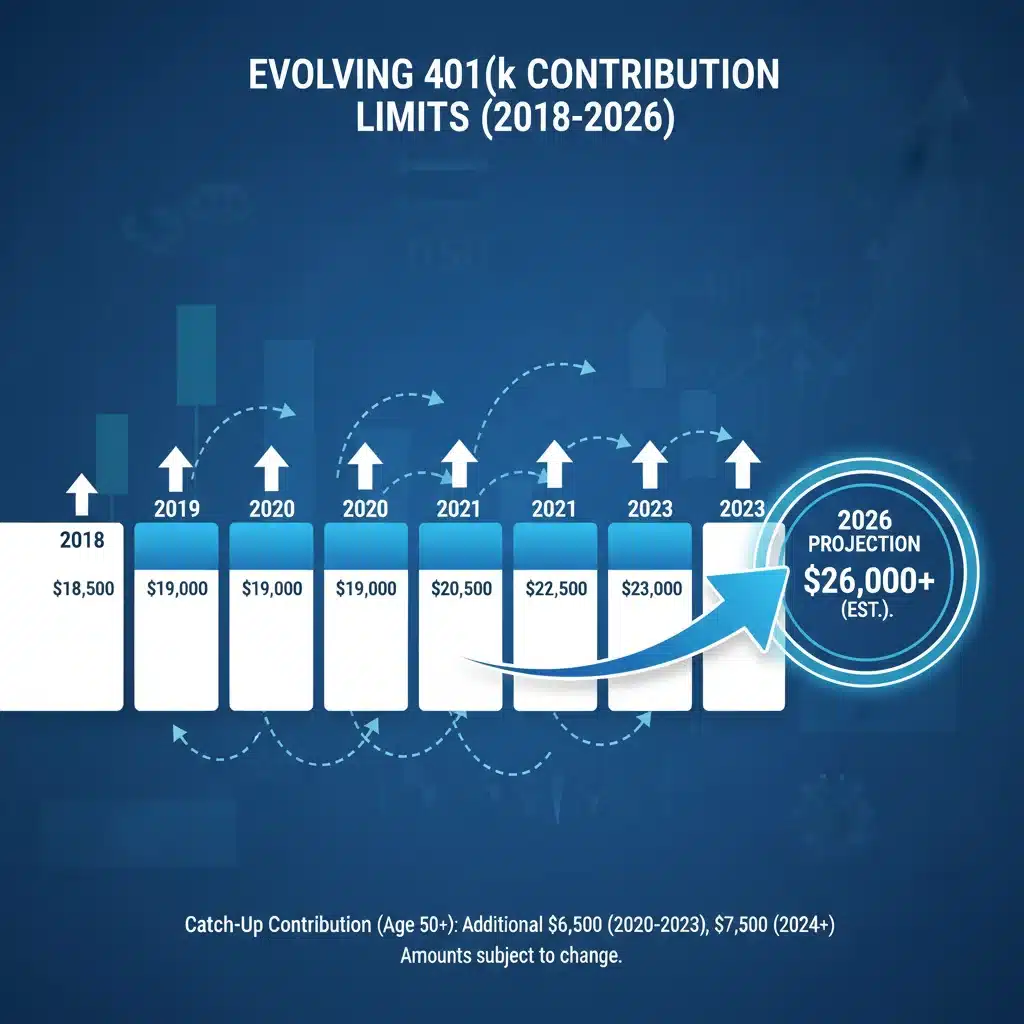

The IRS typically announces the new contribution limits in the late fall of the preceding year. While we don’t have the definitive figures for 401k contribution limits 2026 yet, historical trends provide a strong basis for projection. Over the past few years, we’ve seen consistent increases, reflecting ongoing inflation. For instance, the general employee contribution limit for 401(k) plans increased from $20,500 in 2022 to $22,500 in 2023, and further to $23,000 in 2024. This upward trajectory is expected to continue into 2026, making it vital to anticipate and prepare for these changes.

Projecting the 401k Contribution Limits 2026

Given the annual adjustments by the IRS, projecting the 401k contribution limits 2026 involves analyzing historical data and current economic forecasts, particularly inflation rates. While these are estimates and subject to change, they provide a valuable benchmark for your forward-looking financial planning.

Typically, the IRS uses the Consumer Price Index for All Urban Consumers (CPI-U) to make these adjustments. If inflation continues at its recent pace, or even moderates slightly, we can anticipate a further increase in the standard employee contribution limit. Based on recent trends and economic predictions, it is reasonable to expect the general employee contribution limit for 401(k) plans to be in the range of $24,000 to $25,000 for 2026. This is a significant figure, representing a substantial opportunity for individuals to save more for their future.

It’s important to remember that this projection is for the employee deferral limit. There are other layers to 401(k) contributions, including employer contributions (matching or profit-sharing) and the overall limit for combined employee and employer contributions, often referred to as the Section 415 limit. This overall limit is also subject to annual adjustments and will likely see a corresponding increase. For 2024, the overall limit was $69,000, or $76,500 including catch-up contributions. For 2026, we could see this overall limit approach or even exceed $70,000 to $72,000 before considering catch-up contributions.

These projected increases underscore the importance of regularly reviewing your contribution strategy. What might have been a maximum contribution in previous years could be less than the optimal amount in 2026. Financial advisors often recommend aiming to contribute at least enough to receive your employer’s full matching contribution, as this is essentially free money. Beyond that, striving to reach the maximum employee deferral limit, especially the projected 401k contribution limits 2026, can significantly boost your retirement savings trajectory.

Keeping an eye on economic news and official IRS announcements as 2025 progresses will be key to confirming these projections. However, starting your planning with these estimated figures allows you to adjust your budget and investment strategy proactively, rather than reactively.

The Power of Catch-Up Contributions in 2026

For those aged 50 and over, the opportunity to make catch-up contributions is a powerful tool to accelerate retirement savings. These additional contributions allow older workers to contribute above the standard limit, recognizing that they may have less time to save or need to compensate for periods when they couldn’t contribute as much. The catch-up contribution limit is also adjusted annually by the IRS, and it’s a crucial element of the overall 401k contribution limits 2026 discussion.

In recent years, the catch-up contribution limit has also seen increases. For 2024, it stood at $7,500. Based on inflation adjustments, it’s reasonable to project that the catch-up contribution limit for 2026 could increase to $8,000 or even $8,500. This means that individuals aged 50 and older could potentially contribute a combined total of around $32,000 to $33,500 to their 401(k) in 2026 (projected standard limit plus projected catch-up limit).

This additional saving capacity is particularly beneficial for individuals who started saving later in their careers, experienced career breaks, or simply wish to supercharge their retirement funds in their prime earning years. Maximizing both the standard and catch-up contributions annually can make a substantial difference in the ultimate size of one’s retirement nest egg. For example, contributing an extra $8,000 per year for 10 years, assuming a modest 6% annual return, could add over $100,000 to your retirement savings.

It’s important to note that catch-up contributions are separate from the regular employee deferral limit. If you are 50 or older, you can contribute up to the standard limit AND the catch-up limit. This dual opportunity provides a significant advantage that should not be overlooked. Employers do not typically match catch-up contributions, but the tax benefits and compounded growth still make them an incredibly valuable component of retirement planning.

When planning for the 401k contribution limits 2026, those approaching or over age 50 should specifically factor in the projected catch-up contribution amount. This foresight allows for budgeting and salary deferral adjustments to take full advantage of this accelerated savings mechanism. Consulting with a financial advisor can help you integrate catch-up contributions effectively into your broader retirement strategy, especially when balancing multiple savings vehicles.

Strategies to Maximize Your 401(k) Contributions for 2026

Knowing the projected 401k contribution limits 2026 is only the first step. The next is to develop a strategic approach to maximize your contributions. Here are several actionable strategies to ensure you’re making the most of your 401(k) plan:

1. Automate Your Contributions and Increase Regularly

The easiest way to consistently contribute to your 401(k) is through automatic payroll deductions. Set it and forget it. As the 401k contribution limits 2026 increase, make it a habit to review your contribution percentage annually and adjust it upwards. Even a small increase, like 1% or 2% of your salary each year, can significantly impact your long-term savings without a major hit to your take-home pay.

2. Always Capture the Employer Match

This cannot be stressed enough: if your employer offers a matching contribution, contribute at least enough to receive the full match. This is free money and represents an immediate, guaranteed return on your investment. Failing to do so is leaving money on the table, directly impacting your potential retirement wealth. Understand your employer’s matching formula and ensure your contributions meet the threshold.

3. Front-Load Your Contributions (if feasible)

Some individuals prefer to front-load their 401(k) contributions, meaning they contribute a higher percentage early in the year to reach the maximum limit sooner. This strategy can be beneficial if your plan allows it and if you are confident you will remain employed throughout the year, as it allows your money more time to grow within the tax-advantaged account. However, be cautious if your employer’s match is calculated per paycheck; ensure you don’t hit the maximum too early and miss out on later match opportunities. Some plans have a ‘true-up’ feature to account for this.

4. Utilize Catch-Up Contributions if Age-Eligible

As discussed, if you are 50 or older, prioritize making catch-up contributions. This extra allowance is a golden opportunity to boost your savings in the years leading up to retirement. Integrate the projected 2026 catch-up limit into your financial plan.

5. Understand Your Plan’s Vesting Schedule

Employer contributions often come with a vesting schedule, meaning you must work for a certain period before their contributions become fully yours. Be aware of your plan’s vesting schedule, especially if you are considering a job change. Understanding this can influence your contribution strategy and job mobility decisions.

6. Diversify Your Investments Within Your 401(k)

While maximizing contributions is vital, so is how you invest that money. Ensure your 401(k) portfolio is properly diversified and aligned with your risk tolerance and time horizon. Regularly review your investment options and rebalance your portfolio as needed. Don’t let your contributions sit in a low-growth fund if you have a long time horizon.

7. Consider a Roth 401(k) Option

If your plan offers a Roth 401(k) option, consider its benefits. Contributions are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. This can be particularly advantageous if you expect to be in a higher tax bracket in retirement than you are now. The 401k contribution limits 2026 apply to both traditional and Roth 401(k) contributions collectively.

8. Review Your Overall Financial Plan

Your 401(k) is one piece of a larger financial puzzle. Ensure your contributions align with your overall retirement goals, debt management strategies, and other savings objectives (e.g., emergency fund, college savings). A holistic approach ensures your 401(k) strategy complements your broader financial well-being.

By implementing these strategies, you can proactively prepare for the 401k contribution limits 2026 and position yourself for a more secure and prosperous retirement.

The Impact of Economic Factors on 401(k) Limits and Your Savings

The determination of 401k contribution limits 2026 is not an arbitrary decision; it’s a direct result of economic factors, predominantly inflation. Understanding this relationship can help individuals better anticipate future changes and adjust their financial planning accordingly. When inflation is high, the cost of living increases, and the IRS typically raises contribution limits to maintain the purchasing power of retirement savings.

However, economic conditions affect more than just the limits. They also influence the growth of your investments within the 401(k). A strong economy, often characterized by low unemployment and robust corporate earnings, can lead to higher stock market returns, boosting your account balance. Conversely, economic downturns can lead to market volatility and slower growth, or even temporary declines.

Interest rates also play a role, particularly for bond investments within your 401(k) and for the broader economic environment that influences stock performance. Higher interest rates can make fixed-income investments more attractive but can also dampen economic growth, potentially affecting equity markets.

For individuals, this means that while maximizing contributions to the 401k contribution limits 2026 is crucial, it’s equally important to stay informed about the broader economic landscape. Diversifying your portfolio across different asset classes (stocks, bonds, real estate, etc.) can help mitigate risks associated with economic fluctuations. A well-diversified portfolio is designed to perform relatively well across various economic cycles.

Furthermore, periods of high inflation, which often trigger increases in 401(k) limits, also mean that your future retirement expenses are likely to be higher. This reinforces the need to not only contribute the maximum allowed but also to ensure your investments are growing at a rate that outpaces inflation. Regularly reviewing your investment strategy with a financial professional can help you navigate these complex economic currents.

The interplay between economic factors, IRS regulations, and your personal financial decisions is intricate. By understanding how these elements connect, you can make more informed choices regarding your 401(k) and ensure your retirement savings strategy is resilient against unforeseen economic shifts. Proactive engagement with your financial plan, especially in light of the evolving 401k contribution limits 2026, is your best defense.

Common Misconceptions and FAQs About 401(k) Limits

Despite their widespread use, 401(k) plans and their contribution limits are often subject to various misconceptions. Clearing these up is vital for effective retirement planning, especially when considering the 401k contribution limits 2026.

Misconception 1: The limit applies to all my retirement accounts.

Reality: The standard 401(k) contribution limit applies specifically to your 401(k), 403(b), and most 457 plans. It does not include contributions to Traditional or Roth IRAs, which have their own separate limits. However, the overall limit (Section 415 limit) does include all contributions to your 401(k) plan, including employer contributions.

Misconception 2: If I change jobs, my contribution limit resets.

Reality: The employee deferral limit for a 401(k) is per individual, not per plan. If you contribute $10,000 to one 401(k) plan and then switch jobs, you can only contribute the remaining amount of the annual limit (e.g., $14,000 if the limit is $24,000) to your new employer’s 401(k) plan for that year. Exceeding this combined limit across multiple plans can lead to tax penalties.

Misconception 3: Employer contributions count towards my personal contribution limit.

Reality: Your personal employee deferral limit (and catch-up contribution limit) is separate from your employer’s contributions (match or profit-sharing). Employer contributions count towards the overall Section 415 limit, which is much higher. You can contribute up to your personal limit, and your employer can contribute on top of that, up to the overall limit.

Misconception 4: I can only contribute a percentage of my salary.

Reality: While many plans allow you to set a percentage, the IRS limit is a dollar amount. You can contribute up to that dollar amount, regardless of what percentage of your salary it represents. For high-income earners, this often means hitting the maximum dollar amount long before reaching a high percentage of their salary.

Misconception 5: I should only contribute if my employer offers a match.

Reality: While maximizing an employer match is crucial, contributing to a 401(k) is beneficial even without a match due to the tax advantages (pre-tax contributions and tax-deferred growth) and the disciplined savings approach it encourages. It’s often one of the best vehicles for long-term retirement savings.

FAQs about 401(k) Contribution Limits 2026:

- When will the official 401k contribution limits 2026 be announced?

The IRS typically announces the official limits for the upcoming year in the late fall of the preceding year. So, expect the 2026 limits to be released in late 2025. - What happens if I over-contribute to my 401(k)?

If you contribute more than the allowable limit, the excess contributions are taxable in the year they were contributed and again when distributed. It’s crucial to correct over-contributions by withdrawing the excess amount (and any earnings on it) by the tax filing deadline to avoid penalties. - Are Roth 401(k) contributions subject to the same limits?

Yes, the standard employee deferral limit (and catch-up limit) for 2026 applies to your combined contributions to traditional and Roth 401(k) accounts. You cannot contribute the maximum to both independently. - Does my income affect my ability to contribute to a 401(k)?

Unlike Roth IRAs, there are no income limitations to contribute to a traditional or Roth 401(k). However, highly compensated employees (HCEs) may be subject to certain non-discrimination testing rules by their plan, which could limit their contributions in some cases, though this is less common for individual deferrals up to the IRS maximum. - Can I contribute to both a 401(k) and an IRA?

Absolutely! You can contribute to both a 401(k) and an IRA (Traditional or Roth) in the same year, provided you meet the eligibility requirements for each. Each account has its own separate contribution limits.

Understanding these points will help you navigate your 401(k) contributions with greater confidence and avoid common pitfalls as you plan for the 401k contribution limits 2026.

Conclusion: Proactive Planning for Your Retirement Future

As we’ve explored, understanding and strategically planning for the 401k contribution limits 2026 is a cornerstone of effective retirement planning. While the official numbers are still to be released, informed projections based on historical trends and economic forecasts provide a solid foundation for your financial strategy. The anticipated increases in both standard and catch-up contribution limits present a significant opportunity to accelerate your savings and build a more robust retirement nest egg.

The key takeaway is the importance of proactive engagement with your retirement plan. Don’t wait for the official announcements in late 2025 to start thinking about your 2026 contributions. Begin now by reviewing your current contributions, assessing your employer’s matching policy, and considering whether you are on track to meet your retirement goals. For those aged 50 and over, the catch-up contributions are an invaluable tool that should be fully utilized.

Remember that your 401(k) is a powerful, tax-advantaged vehicle designed to help you achieve financial independence in retirement. By consistently contributing, leveraging employer matches, diversifying your investments, and staying informed about IRS changes like the 401k contribution limits 2026, you are taking concrete steps towards securing a comfortable and worry-free future. Consulting with a qualified financial advisor can provide personalized guidance, helping you tailor these strategies to your unique financial situation and long-term aspirations. Start planning today, and make 2026 a landmark year for your retirement savings.

2026 IRS Tax Code Changes: Small Business Action Plan

2026 IRS Tax Code Changes: Small Business Action Plan  Bond yield volatility effects on mortgage rates US: risks?

Bond yield volatility effects on mortgage rates US: risks?